Happy Sunday Friends!

With the inception of the pandemic, borrowers have largely been wrestling with financial distress, compelling fintech companies like SoFi technologies, which banks on student loan financing, to largely reimagine their business model. SoFi has moved away from its core business over the past three years, instead casting a wider net, extending its services to include diverse financial products, personal loans, and its banking-as-a-service business targeting enterprise customers. In 2023, SoFi has had to grapple with mounting external pressures emanating from a slowing economy.

The housing market has skidded to a standstill, and personal loan origination has taken a downturn due to a weakening job market. Despite a barrage of these challenges, SoFi has defied expectations by not only bolstering growth but also delivering profits. Last week, SoFi received a significant shot in the arm. The newly minted debt ceiling agreement contains a provision for ending the student debt moratorium and cancellation, offering a potential boon to SoFi's original core business. So how do these changes intersect with SoFi's long-term growth trajectory? Let's take a look.

Silver Lining

Student loan payments and accruing interest have been on hold since the pandemic's onset, a hiatus initially implemented and extended under former President Donald Trump, and subsequently lengthened under President Biden. This sequence of student loan pauses – eight in total over the past three years – has substantially impacted the student loan market.

As a result, SoFi's loan originations have plummeted from $1.04 billion in the first quarter of 2021 to just $525.37 million in the equivalent period in 2023, a staggering 50% decline. SoFi beehives that the federal freeze has cost the company between $150 million and $200 million in revenues, and had anticipated losing another $30 million as a result of the 8th extension.

However, things took a dramatic twist last Sunday with the finalization of the debt ceiling deal between President Biden and House Speaker Kevin McCarthy. The agreement will resume student loan payments and interest accrual in late August. McCarthy indicated that the student loan pause would be “gone within 60 days” of the bill being signed.

SoFi's memberships have surged 300% since the student loan pause was first initiated, so the resumption of payments should be a big boost for the company. While refinancing and originations aren't anticipated to immediately skyrocket (due to a higher interest rate environment), revenues should significantly grow in 2024/25.

Want to Find the Best FinTech Stocks? Try Benzinga

(Offer Expires 06-14-2023)

I use tons of trading software to help me better understand the market and make smarter trading decisions. one thing I love about Benzinga Pro is its versatility. It wasn't built for just one type of trader but for a wide range of experienced investors like myself. I can create custom watchlists, and then quickly monitor the performance of my investments.

Some great news – Benzinga is giving all subspac readers a free two week trial!

Loan Quality Concerns

Two significant concerns have been casting a shadow over SoFi's valuation: the quality of its personal loans and the quality of the loans related to mortgage originations. As the student loan moratorium continued, personal loans emerged as the primary constituent of SoFi's loan originations.

Meanwhile, mortgage originations experienced a decline, largely due to rising interest rates. Critics have questioned the stability of these personal loans, particularly in light of an increasingly volatile job market. Furthermore, market participants were skeptical about the company's loan book, given that it hadn't sold any loans, questioning if there were any issues related to fair value accounting.

In its latest earnings call, SoFi's management team provided insights into the process, helping soothe concerns. According to management, SoFi rejects over two-thirds of its personal loan applications and evaluates the applicant on numerous measures such as the underlying cash flow, cash-to-debt ratio, and other parameters. The company has also adjusted its underwriting parameter in response to the evolving economic landscape to get ahead of the situation.

The management team also clarified that the shift in strategy in selling loans is due to rising rates. Back in 2018, when the Fed suddenly started raising rates, SoFi employed a similar approach of retaining loans that yield more than 6%, while selling loans that had yields of around 4%. While the operating environment isn't the best for SoFi (given the deterioration of the underlying economy and rising rates), the company is well-positioned to take advantage of the rebound in the economy when interest rates fall next year.

Banking-as-a-Service

Despite the rapidly evolving digital age, around 75-80% of financial institutions still rely on in-house built core banking systems, many of which are relics from the pre-internet era, designed for physical branch banking. This antiquated infrastructure presents a significant opportunity for a platform like the one SoFi envisions. SoFi is looking to capture the burgeoning market space representing a $7 trillion opportunity with its Technisys and Galileo Banking-as-a-Service (BaaS) platform.

The company is currently in discussion with over a dozen financial institutions, leveraging its technology slack to maintain real-time asset and liability data (something that the likes of ill-fated banks like Silicon Valley Bank and First Republic struggled with in recent months). With interest in SoFi's technology platform growing exponentially, SoFi could become the Amazon Web Services (AWS) of the fintech world.

Financials and Valuation

SoFi showcased robust performance in the first quarter of 2023, adding 433,000 new members. Although the annual growth has moderated from 110% in 2021 and 70% in 2022 to 46% in 2023, the membership base has surged to over 5.7 million. This marks a five-fold increase since 2020 and a near tripling since 2021. While the Galileo Accounts registered a minor dip quarter-over-quarter, they still exhibited a 15% annual growth, amounting to 126 million accounts.

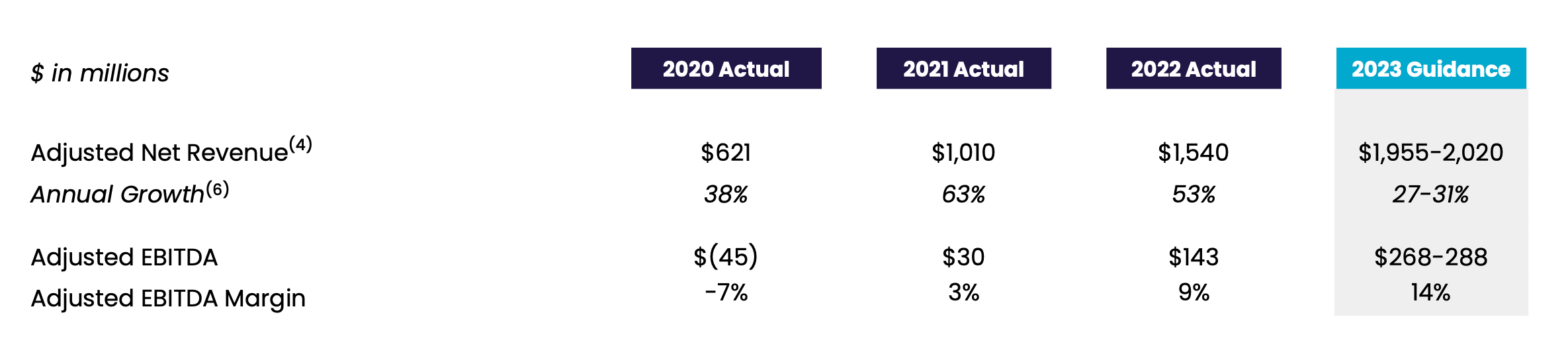

Since the onset of the pandemic, the platform has expanded four-fold and nearly doubled since 2021. The company's revenue trajectory remained strong, reaching $460 million in Q1 2023, a 43% year-over-year increase. The EBITDA for Q1 was $76 million. Both these metrics outperformed the company's prior guidance, which had projected revenues between $430-$440 million and EBITDA between $40-$45 million. This performance led to a rally in SoFi's shares.

In the second quarter, SoFi predicts revenues ranging between $470 and $480 million, with the EBITDA anticipated to be between $50 and $60 million. The company also increased its full-year guidance, expecting revenues between $1.955 billion and $2.02 billion (indicating a growth rate of 27-31%) and an EBITDA between $268 and $288 million. This suggests an EBITDA margin of around 14%, a marked improvement from 9% in 2022.

Once the student loan pause and forgiveness are indeed repealed, SoFi could witness an additional revenue stream between $300 million and $500 million for the full year. This assumes two-quarters of revenues from student loans and a potential addition of $100-$165 million to the EBITDA. At present, SoFi trades at roughly $7.05 per share, giving it a market capitalization of about $6.46 billion.

Based on the forecasted revenue of $2 billion, the stock is likely to trade at approximately 3.23x sales. While this multiple may seem low compared to the high valuations observed in 2020/21, it is worth noting the company is still grappling with economic challenges that could worsen before improving.

However, it is crucial to consider that SoFi, due to its high exposure to interest rates, is well-positioned to benefit once the economy rebounds. Therefore, as the macroeconomic conditions improve in the medium term, SoFi's stock is expected to perform significantly better.

Bottom Line

SoFi's strategic diversification and robust financial health position it well to navigate through current economic headwinds. The imminent return of student loan payments could significantly boost its revenues, potentially transforming the challenges of the past into growth opportunities. Furthermore, the expansion of its Banking-as-a-Service segment indicates its readiness to seize the future of fintech. While the road ahead may present obstacles, SoFi's adaptability and resilience make it a promising prospect in the long term.

Source: Beyond Student Loans