- Cheering for the underdog works in Disney movies.

- In SPACs, the overdogs are better bets.

- 5 SPAC warrants worth owning today.

Underdogs vs. Overdogs

If you want to place a bet on who comes out on top in the next Disney (DIS) cartoon, bet on plucky little upstarts. The smaller, weaker outcasts defy the odds and win the day pretty much every day. That’s how it works in the movies. It’s not how it works in the world generally or in special purpose acquisition companies (SPACs). As I wrote in SPAC Size Matters, the best opportunities are in the biggest SPACs.

Meet today’s underdogs

There are 29 SPACs without announced business combinations with separately trading warrants under $0.70. All of them fit neatly into three categories: SPACs that include dilutive rights as part of their capital structure, undersized SPACs, and SPACs focused on cannabis (some fit into two or even all three categories). None are particularly promising. My business partner once said,

Where should we look for investment opportunities? Where no one else is looking and where everyone else is panicking.

That is almost always right, but isn’t right for SPACs. In SPACs, the ignored or hated sponsors actually are the worst. That is for two reasons. One, SPAC size is based on a real market test: how much can sponsors raise? Two, SPAC sponsors have as much of a marketing role as an investing role between their IPO and de-SPACing. If they are out of favor, they are failing at their marketing role.

A good sponsor is like a good bartender – he gives the people what they want with a smile and without judging. Give them the sector and scale that the market demands. Should customers be more sober and frugal? Those are important virtues; for cultivating virtue I recommend reading Marcus Aurelius, Seneca, and Cato. But that isn’t the job of bartenders or SPAC sponsors; they have the humbler role of offering something that investors want at a price they are willing to pay.

Meet today’s overdogs

Today, there are four SPACs seeking business combinations with over a billion dollars in their trust accounts – PSTHU, CCIVU, BFTU, and WPFU – and all four are worth owning. Based on information and belief, all four are on track to announce business combinations well before their liquidation dates. My confidence in their consummating deals leads me to focus on their warrants. One can buy WPF+ warrants in the open market today; for the other three, one can buy units and then split them when that option becomes available in the weeks ahead.

These overdogs will be able to buy companies that are already big enough to absorb significant public company costs related to reporting and regulatory compliance. Their underwriters are meaningfully incented to aid them in lining up high-quality deals. Their fame opens doors. When they launched, there was wall-to-wall coverage on Bloomberg (itself a potential SPAC target) and CNBC. All that is free/earned media that doesn’t cost sponsors a penny but catches the attention of potential targets. In the SPAC world, the bigger you are, the harder targets fall for you.

The rockier the better

Volatility serves Pershing well. The rougher the markets, the more willing the sellers. If there is a big sector rotation, Pershing can avoid whatever moves out of favor and jump on whatever moves in favor. If the market implodes as it did in March, then Pershing is still protected by the cash in trust. The more that capital in general dries up, the comparatively dearer Pershing’s capital becomes.

2 of the most recent overdogs

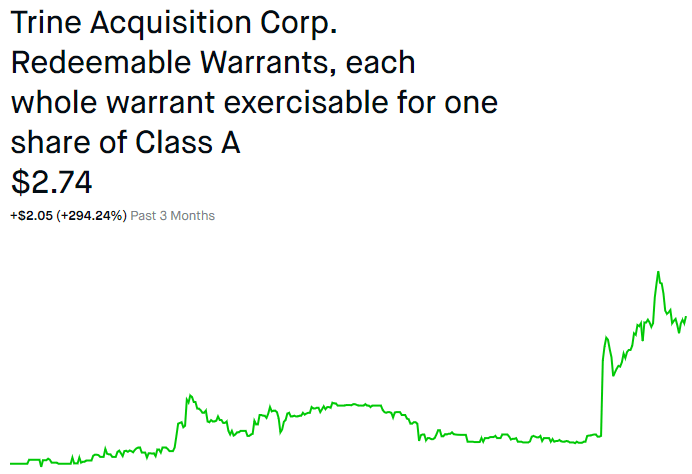

What has happened to the last two overdogs? It is useful to look at the two most recent overdog SPAC ideas – Trine (TRNE) and Kensington (KCAC). In the early summer, Trine was a big SPAC with a top tier sponsor likely to quickly announce a good deal. Security holders risked next to nothing. At the time I wrote that,

His prospects of finding a deal are over 99%. He has been an active and successful dealmaker his entire career; it is reasonable to assume that he already has potential targets lined up. While he had 24 months to find a deal, recent SPACs have been going much quicker, with the average SPAC pre-deal lifespan cut in half to about a year. He originally expected to find a deal within six months. That has been delayed but will probably not be delayed much longer. If he is able to find something, the warrants could be the best leveraged way to get exposure to Trine.

Since then, they announced their acquisition of Desktop Metal and their TRNE+ warrants more than doubled.

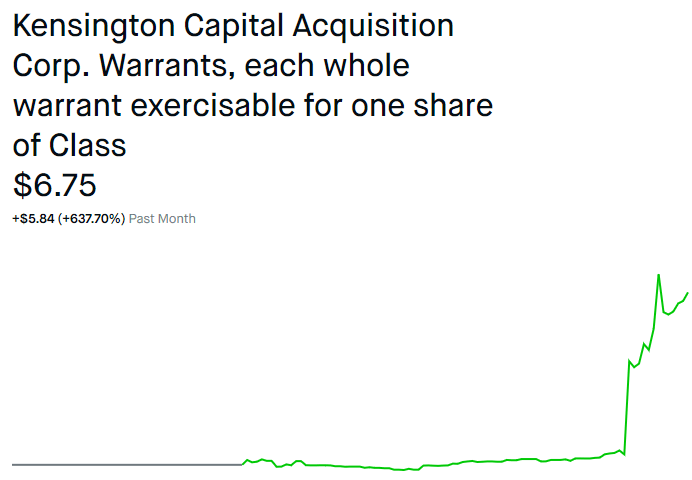

Around the same time in early summer, Kensington was in the same situation: another big SPAC with top tier sponsors likely to quickly announce a good deal. Again, security holders risked next to nothing. I wrote then and still believe now that,

As many ESG mandated investors allocate based on market cap, they allocate more capital the higher these EV company stocks rise. That in turn improves ESG performance drawing more capital. Now over $40 trillion is invested based in part on ESG criteria. It can’t all get invested in Tesla (TSLA), so each one of these EV companies will have a flood of price-insensitive investors ready to invest. Nikola (NKLA) demonstrated it, Fisker (SPAQ) reinforced it, and KCAC can be the next big beneficiary which is why I own their KCACU units. These include a KCAC share as well as a half of a KCAC+ warrant. This is my candidate for the next automotive SPAC to pop 50% like SPAQ did, to impress retail speculators, and to take down their share of the $40 trillion ESG money pile.

What happened? Their history has been short but eventful. Their KCAC+ warrants just started trading separately last month. Since then, the SPAC announced a deal with QuantumScape. I’ve been looking at this company for months and am thrilled that they reached a deal with Kensington. Apparently, the market agrees with the warrants up over 600% so far.

What’s next?

The SPAC overdogs will take advantage of this strong market for SPACs. They will move fast, taking less than half of their time windows. The biggest big dog, Pershing Square Tontine, will announce a deal by year-end. Sometime by the end of December 2020, they will sign a definitive deal to buy a big company such as Bloomberg and shareholders will enthusiastically vote for the deal with only de minimis redemptions.

Units will pop to at least $30 per unit. From today’s price, that will be a great risk:reward and IRR. The warrants will be even better. There is little incremental downside in the warrants relative to the equity because there isn’t nearly as much difficulty in finding a big deal. There is such a finite number of companies for them to choose between that they will be able to wrap up their pick within a very few months. There are tens of thousands of targets for small SPACs but only tens of targets for the big ones. Many will be receptive.

Conclusion

Don’t overthink SPACs. I like nothing better than discovering some obscure, unfollowed gem of a public company that few others have even heard of, but that is not how to approach SPAC opportunities. I get no points for creativity for investing in PSTHU, CCIVU, BFTU, and WPFU, but they are all safe and potentially extremely profitable. A portfolio equally weighted among these four is likely to outperform the S&P 500 (SPY) over the course of the next twelve months regardless of what the broader market does.

If it implodes, the four SPACs will decline far less due to the redemption rights and their cash in trust. If the market goes sideways, the four overdogs will easily beat it when they pop on deal announcements. If the market rockets, so will these four. They will announce deals, probably in hot sectors, and capture the difference in multiples between the private and public markets. Whether the S&P 500 wins, loses, or draws, the four biggest SPACs seeking deals are bound to win and win big.

Postscript

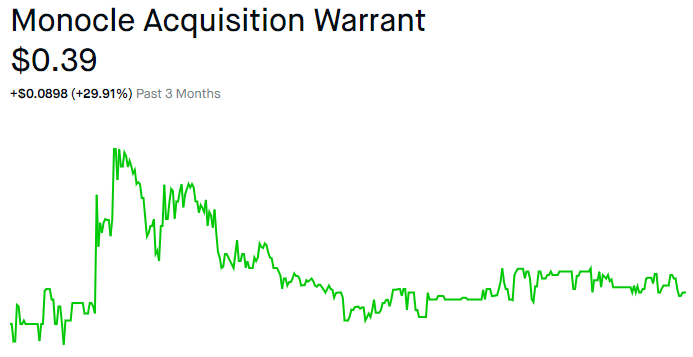

Careful readers will note that in the bullet points I offered “5 SPAC warrants worth owning today” and have only mentioned four. So if you’re still reading, here is number five. There is one smaller, less widely owned SPAC warrant that I own and that you should, too: Monocle (MNCLW). (See further discussion of Monocle in link.)

I’m involved every which way – as an owner of units, equity, and warrants and a sponsor is a family member and business partner – so take this with a big grain of salt (or, er, um, many big grains of salt). But time is short and warrant holders as well as other security holders could profit from a re-cut deal within the next few months. Given the fact that their deal target AerSale is as impacted as any SPAC target by Covid, the market’s reaction to the deal has been tepid so far. The deal risks substantial redemptions without substantial changes. Strategically, the deal makes sense but only at the right price. Within the next few months, warrant holders could benefit from the right deal and the right price. Next time there is news, you could get amply rewarded for reading all the way to the end!

I’m involved every which way – as an owner of units, equity, and warrants and a sponsor is a family member and business partner – so take this with a big grain of salt (or, er, um, many big grains of salt). But time is short and warrant holders as well as other security holders could profit from a re-cut deal within the next few months. Given the fact that their deal target AerSale is as impacted as any SPAC target by Covid, the market’s reaction to the deal has been tepid so far. The deal risks substantial redemptions without substantial changes. Strategically, the deal makes sense but only at the right price. Within the next few months, warrant holders could benefit from the right deal and the right price. Next time there is news, you could get amply rewarded for reading all the way to the end!

Source: Seeking Alpha – It Pays To Be A (SPAC) Winner