Happy Sunday Friends!

The pandemic hit the eatertainment industry hard, pushing many to the brink. But as the world started to bounce back, so did the demand for fun dining experiences. Pinstripes, a bowling and dining chain operator, is riding this wave and has big plans after going public through a SPAC. Yet, the company is an underdog when stacked against some of its peers in the game. The company has a unique spin on things, but with the competition heating up, Can Pinstripes carve out a niche and satisfy the appetite of its investors?

Not Just Pins and Pasta

For those unfamiliar with Pinstripes, the company is part of the “eatertainment” wave, a blend of dining and entertainment, that’s been sweeping across America. While the concept isn’t novel—think Chuck E Cheese in 1977 and Dave & Buster’s in 1982—the recent surge in interest is still noteworthy.

After a pandemic-induced hiatus, Americans, starved for fresh experiences, are flocking to these venues to eat, play, and reconnect with their friends and family. The Gen Z and Millennial crowd are the ones who are propelling this industry. The reason this isn’t surprising is that this crowd isn’t just looking for a place to hang out but is rather scouting for the next viral backdrop for their Instagram and TikTok posts.

For them, the ambiance, the food, and the entire experience need to be share-worthy. And they’re willing to spend more for it, often choosing eatertainment venues over traditional ones. Historically, the eatertainment industry leaned heavily on the entertainment aspect, with food often being an afterthought. But times are changing.

Today, there’s a notable shift towards balancing top-notch dining with engaging entertainment. Pinstripes is a great example of this evolution. Three-fourths of the company’s revenues come from its Italian-American food and drink sales, while the remaining is from games. While customers may come in for bowling and bocce, they stay for the handcrafted dishes, locally sourced ingredients, rotating craft beers, and custom menus that resonate with the location-specific demographic.

Want to Find the Best De-SPACs? Try Benzinga

(Offer Expires 10-10-2023)

I use tons of trading software to help me better understand the market and make smarter trading decisions. One thing I love about Benzinga Pro is its versatility. It wasn’t built for just one type of trader but for a wide range of experienced investors like myself. I can create custom watchlists, and then quickly monitor the performance of my investments.

Some great news – Benzinga is giving all subspac readers a free two week trial!

Striking Ambitions

Since its inception in 2008, Pinstripes has carved a niche in the eatertainment industry, building out 13 locations across eight states, boasting average unit volumes over $8 million. The company’s recipe for steady growth is a blend of aesthetic venues, Italian-American cuisine, bowling, bocce, and banquet spaces for private events. Interestingly, while bowling and dining is the company’s mainstay, it’s the private events corporate, and social gatherings that rake in most of the revenue.

With eyes set on expansion, Pinstripes is looking to nearly double its venues to 25, primarily targeting suburban America, through its SPAC merger. However, Pinstripes has a long way to go, especially when compared to its peers in the industry.

For instance, while Pinstripes’ average revenue per location stands at $8 million, leaders in the space like Topgolf, Lifetime, and Dave & Busters pull in $17.1 million, $11.3 million, and $11 million respectively. This disparity isn’t just in revenue, but also in reach. Topgolf boasts 82 venues and Dave & Busters, a whopping 154, both dwarfing Pinstripes’ 13 outlets.

Pinstripes is forecasting filling domestic whitespace with nearly 150 outlets, a tenfold increase from its current footprint. This is a bold target, especially considering their modest growth over the past 15 years. But in the end, it’s not just about ambition—it’s about market demand and outpacing the competition. Only time will tell if Pinstripes can strike the right balance and expand as envisioned.

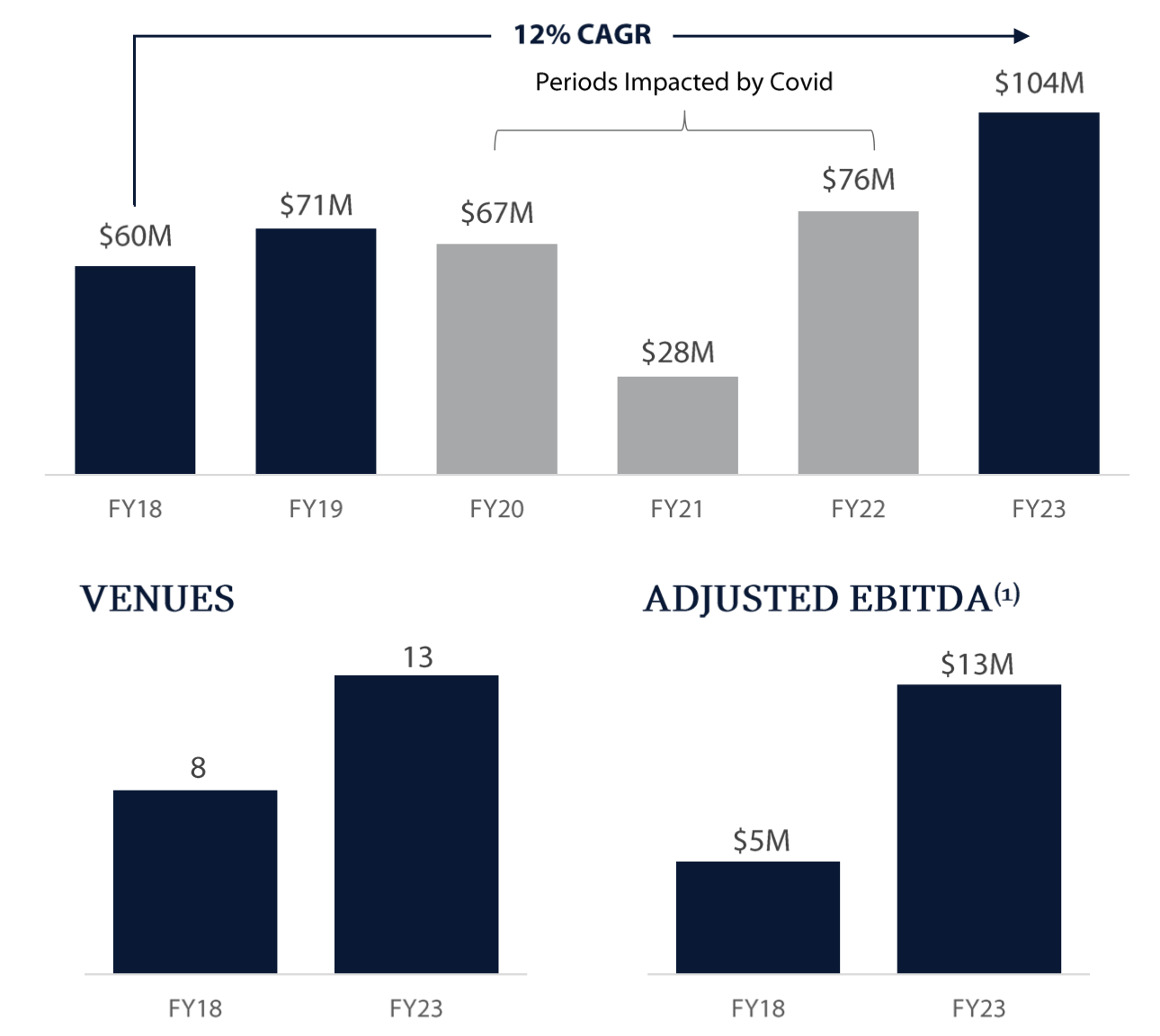

Financials and Valuation

Pinstripes has shown modest growth between 2018 to 2023, with revenues jumping from $60 million to $104 million. The uptick in revenue can largely be attributed due to an increase in locations, from 8 to 13 over five years. Concurrently, its EBITDA also rose, moving from $5 million to $13 million.

The elephant in the room is the impact of the pandemic, where Pinstripes faced a tough stretch, with revenues plummeting to $28 million in 2021 and only modestly growing to $76 million, displaying modest growth compared to the $71 million the company made pre-pandemic. Looking forward, Pinstripes has big plans, aiming to nearly double their venues to 25, forecasting sales between $185 and $195 million and an EBITDA ranging from $30 to $33 million.

These projections hinge on Pinstripes securing the full $75 million in gross proceeds, which includes $40 million from the SPAC trust, a $20 million direct investment from Middleton Partners, and an additional $15 million from an Incremental PIPE. However, SPAC deals can be unpredictable, and High redemptions could end up leaving Pinstripes cash-strapped, a risky position for a company that leans on leverage for expansion.

Reflecting market sentiments, Banyan Acquisition has recently adjusted Pinstripes’ merger valuation from an initial $520 million to about $480 million. This revised valuation, translating to a 2.5x 2024 Price/Sales multiple, seems reasonable when looking at the company’s peers in the industry. However, much of this valuation will depend on the company’s planned aggressive expansion. Only the coming quarters will reveal if this strategy pays off.

Bottom Line

The pandemic has reshaped the eatertainment landscape, with Millennials and Gen Z driving a hunger for fresh experiences. Pinstripes, blending dining with bowling, is looking to ride this wave, gearing up for a significant expansion post its SPAC deal. However, the company currently trailing behind industry peers in both unit performance and operational scale. The company’s valuation hinges heavily on replicating its current successes in new venues. Only time will tell if the company can deliver on its promise and truly create value.

Source: Rolling with Ambition