Hello Friends!

SPAC critics often argue the businesses that go public through the vehicle create no long-term value but instead act as a means to create exit liquidity for founders and existing investors at the expense of unsuspecting retail investors. This is at least partly true for the handful of companies that have gone bankrupt under a year after going public. However, long before SPACs gained the reputation of being an instrument to raise money for zero-revenue companies with no prospective future, they were considered a viable alternative to an IPO.

With that in mind, let's take a look at a company that went public long before the SPAC boom and what prospective returns are on offer for long-term investors looking at similar businesses.

Market Monopoly

OneSpaWorld is unlike many of the flashy upstart EV or Space companies that went public through a SPAC in the fact that it isn't very well known despite its scale and market domination. The company hit public markets through a SPAC merger in 2019, long before the blank-cheque boom launched the vehicle into the crosshairs of mainstream investors. For the vast majority of investors who don't know about OneSpaWorld, the company essentially operates health and wellness onboard cruise ships and resorts worldwide.

The company achieves this by providing professional staff and resources that operate from the cruise line properties under a revenue-sharing agreement. This enables the company to operate through an asset-light model, bolstering margins and free cash flow. The suite of services on offer includes body, salon, and skin care services, fitness classes, detoxifying programs, and other accompanying services.

What makes OneSpaWorld such an attractive business is its command over the luxury cruise market. OneSpaWorld operates across 179 ships and 51 luxury resorts, including the likes of the Royal Caribbean, Carnival, Disney Cruise Line, Norwegian, and Princess Cruises, among others. This gives the company over 90% of the market share at sea, making it 20x larger than its next closest competitor in the market.

Global Cruise Capacity is also anticipated to grow in the next five years, with the number of passengers annually rising from 29.5 million to 38.7 million. Multiple tailwinds are expected to drive this growth, including an aging global population, Millennials and Gen Z customers seeking luxury experiences, and expansion of the upper-middle class in Asia, all leading to a potentially larger market for OneSpaWorld.

Want to Find the Best De-SPACs? Try Benzinga

(Offer Expires 02-27-2023)

I use tons of trading software to help me better understand the market and make smarter trading decisions. One thing I love about Benzinga Pro is its versatility. It wasn't built for just one type of trader but for a wide range of experienced investors like myself. I can create custom watchlists, and then quickly monitor the performance of my investments.

Some great news – Benzinga is giving all subspac readers a free two week trial!

Lavish Leisure Pursuits

If the sheer dominance and high-margin businesses weren't appealing enough for investors, OneSpaWorld's business has also historically been recession resilient. In fact, this aligns with the dynamics of the global cruise ship passenger growth, which remained robust for 20 years and two recessions (barring the pandemic, which restricted movement and was a black swan event).

A few factors drive the business's resilience, including the predictability of revenues, recurring relationship with cruise operators, and higher spending by passengers on services. First, underlying cruise capacity growth is highly visible and predictable, with order books published every year. Furthermore, OneSpaWorld has had a long-standing relationship with every major cruise operator, giving it an edge.

The average relationship with a cruise line has been 20 years (ranging as high as 29 years with the likes of the Carnival and Royal Caribbean), with a historical contract renewal rate of 94% and a 5-year average contract life. Luxury services and products have also historically outperformed other businesses during periods of slowdown (luxury retailers like LVHM are a prime example of this). Cruise passengers comprise an attractive demographic, with an average income of $114,000, living leisurely, and taking a cruise every three years.

Financials and Valuation

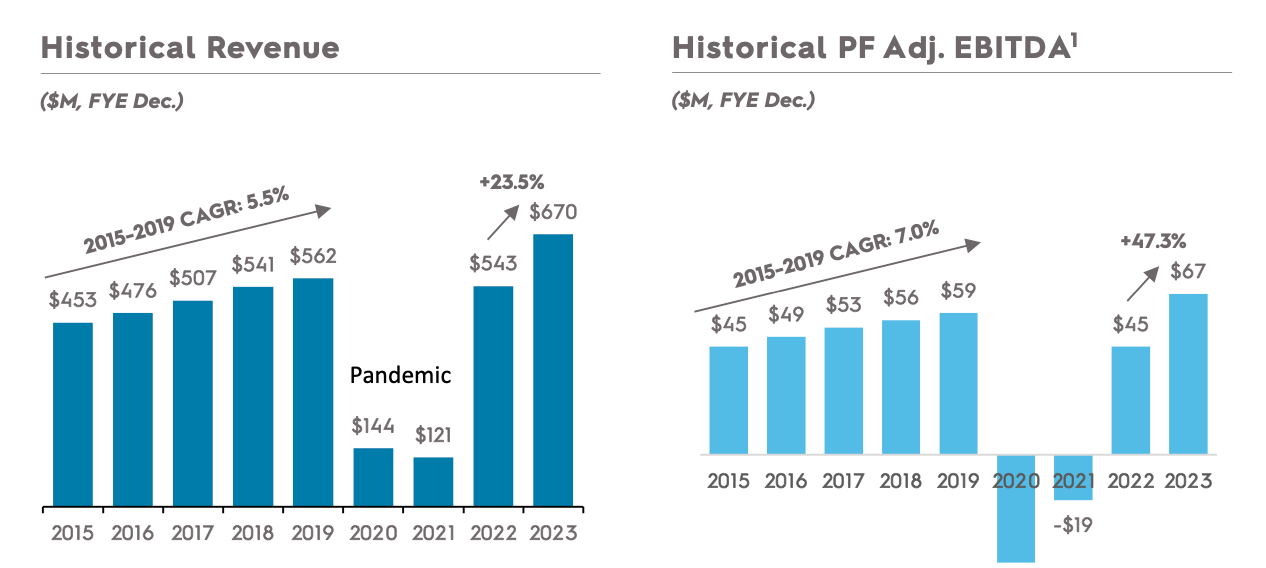

OneSpaWorld generated revenues of $543 million and an EBITDA of $45 million in 2022, which was slightly below the revenues of $562 million seen before the pandemic. However, this was well above the $121 million in revenues and $19 million EBITDA loss in 2021 due to lower passenger volume. Furthermore, with luxury travel expected to return to full strength in 2023, revenues are expected to grow to $670 million, with EBITDA reaching $67 million.

OneSpaWorld also has strong economics since it converts 90% of its EBITDA into free cash flows, with an average capital expenditure of just 1% of revenues. Since the company operates mostly on international waters, its effective tax rate is also low at 2%.

Nearly four years after making its public debut, OneSpaWorld is trading at $10.88, giving it a valuation of close to $1 billion. This company currently trades at a Price/Earnings ratio of 23x, which is favorable considering the long-term tailwinds driving growth. One area of concern is the company's liquidity and balance sheet strength.

OneSpaWorld had cash and borrowing facilities of $57 million at the end of the third quarter, compared to $222 million in long-term debt. Unlike most other De-SPACs, the company doesn't have a problem repaying its debt as a result of strong free cash flows from the business, but a repeat of the shutdown in 2020-21 which halted all operations, could result in the company going out of business.

Bottom Line

While some critics may argue that SPACs create no long-term value, OneSpaWorld's success shows that this is not always the case. OneSpaWorld is a market-dominating business that has historically been recession-resilient, and with tailwinds driving global cruise capacity growth, the company has the potential for long-term success. The company has a strong track record of predictable revenue and a long-standing relationship with major cruise operators. While there are concerns about the company's liquidity and balance sheet strength, its strong free cash flows suggest it is well-positioned to pay off its debt. Overall, OneSpaWorld provides a case study for why SPACs were originally considered a viable alternative to an IPO and can provide long-term value for investors.

Source: Smooth Sailing