Summary

- SPAC Week returns with Joe Crouthers, Co-Founder and CEO of Ceres Group Holdings, who discusses why they’re focused on the plant-touching side of the sector.

- Tying cannabis into traditional business. SPACs more collaborative and less adversarial than traditional IPOs.

- What was irrational exuberance is now based on strong business foundations. The consumerification of cannabis.

SPACs hit the broader markets this year with a bang, and the cannabis industry was no different. Last month we had our first SPAC Week with The Parent Company (OTCQX:GRAMF) and Clever Leaves (NASDAQ:CLVR) and this week we continue with 3 separate episodes for SPAC Week, Part II.

Today we’re joined by Joe Crouthers, Co-Founder and CEO of Ceres Group Holdings and Chairman and CEO of Ceres Acquisition Corp., one of the more visible cannabis SPACs in the industry. Joe is also on the board of directors of Fotmer Life Sciences and was a merger and commodities arbitrage trader before working at Goldman Sachs as a portfolio manager and advisor.

On Tuesday’s episode, we have SPAC superstar Chris DeMuth, who founded Rangeley Capital LLC, a hedge fund focused on SPACs and event driven opportunities and his SA Marketplace Sifting the World, SPAC and event driven research for accredited investors. Wednesday rounds out the week with the return of Michael Auerbach who brings us up to speed with Subversive Real Estate’s (OTCPK:SBVRF) deal with dominant Israeli player, InterCure and updates us on GRAMF.

Topics include:

- After leaving Goldman Sachs in 2016/2017, cannabis felt like a place to do historic good and make good money. A place to accrue profits and more meaning.

- Started distribution business in Northern California; farms were at that point wanting to get rid of trim, they were essentially a brokerage firm for trim. That taught Joe about farms and dispensaries and manufacturers and where there is a lack. Capital was a natural place for Joe to go and what the industry needed, but Joe first learned the business. Tying cannabis into traditional business – not forgetting where it came from but getting it to be an above ground business. Started Ceres in 2017 after listening to what people needed – money and marketing. 12 deals on the private side and then the SPAC side. Only cannabis focused, mostly US, some international. In March announced going public with a SPAC and now looking for targets to de-SPAC.

- Ceres had been investing privately, which was how most of the industry was. Almost no institutional money, stark need for capital, how to bring companies to the next level. For companies equipped to go public, it makes sense. For cannabis sector especially because it allows the investor to wade softly into the deal which makes sense for investors’ hesitation with cannabis. And it makes sense for the operators because it allows them to run a business with more capital. SPAC structure makes more sense for both sides.

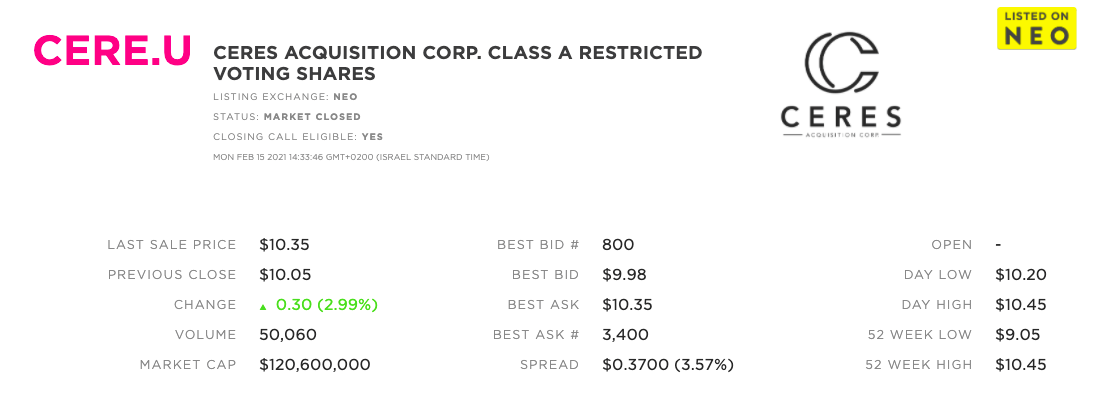

- Ceres went public last March – have 12-24 months to de-SPAC. Speaking to combinations or single companies, sized smaller ($120 million) because they wanted to focus just on cannabis. Looking for businesses between $350 million up to a couple billion in enterprise value, looking at deep, single state operators or multi-state operators. Want to stay close to plant touching side – the core of the industry.

- Cannabis was in a rough patch prior to Covid, and Covid ended up being a real catalyst for cannabis taking off. Regulatory hands were forced. Recent elections was another reinvigoration – since then a number of deals have been announced. Verano, Subversive (OTCQX:SBVCF) deal with The Parent Company (OTCQX:GRAMF), Clever Leaves (CLVR) in South America – it’s forcing people to see how to compete and be opportunistic. It makes SPACs better. Pushes Ceres to be most appealing to targets, not to just look for most appealing target.

- Difference in share price between now and a few years ago – the numbers then were out of whack based on 3 years out revenue expectations. Now many of these companies have proven out this thesis. In 2017-2018 it was irrational exuberance, it came crashing down in 2018-2019 and now companies are justifying their valuations, that brings confidence and legitimization. Fluctuations in share price will continue, but we’re now on a real foundation. Now we have to get basic business enablement tools (280E, etc).

- Thoughts on US market and Canada. Structural issue with Canada because they still don’t have a current way into the US markets. They were the first, which brings some mistakes and growing pains, but there will still be some Canadian winners, especially those making gains internationally in Europe.

- Cannabis in South America – 2 schools of thought: the cheaper you can produce high quality product – what they’re doing in Uruguay, many benefits to growing there. Where is Europe going to get its supply? The other school of thought is Europe cannabis will be grown in Europe and that leaves South America with its own population to rely on for growth. Real sales channels are Australia, Europe and someday Asia. Supplying Europe is the bet, the next couple years will prove out either thesis.

Source: Seeking Alpha- SPAC Week, Part II: Why SPACs Make Sense (Podcast)