Summary

- Remote and hybrid work will be a permanent shift in the labor force.

- WeWork was surprisingly resilient in 2020 and managed to cut billions in excess costs.

- Adam Neumann, the controversial former CEO, has been replaced by Sandeep Mathrani.

- SPAC-IPO structure gives us a unique investment opportunity.

Thesis

COVID-19 led to an explosion in hybrid and remote work, and these changes will be permanent for many companies. WeWork (BOWX) is well-positioned to benefit from shifting labor trends, as it can provide a cheaper office space alternative to enterprise customers. WeWork’s corporate governance and finances are much improved from when the company’s IPO was pulled in 2019, and I believe WeWork is both a fascinating turnaround play and hybrid workforce investment today.

Permanent Remote Labor

COVID-19 forced companies around the world to either adapt to remote working conditions or die. However, while half of US adults have gotten vaccinated and COVID-19 infection rates are dropping across the country, many companies plan to continue remote work options for their employees. A recent survey from Enterprise Technology Research suggests that permanent remote workers will account for over one-third of their companies’ labor forces in 2021. In fact, tech giants Facebook, Twitter, and Microsoft all recently announced that they would let employees stay remote permanently. Why stay remote? Workers are more productive than they were in the office, for starters. No commutes, no “water cooler” discussions, and 24/7 access to one’s workstation have all driven increased productivity for the work-from-home labor force. Geographic hiring constraints have disappeared, so relocating to San Francisco or New York City is no longer a necessity to work for tech and finance giants.

This shift towards remote work benefits workers as much, if not more, than the companies themselves. Half of the current remote labor force would prefer to stay remote for reasons such as flexibility, work-life balance, and convenience even after their offices reopen. While remote work provides several advantages to all parties involved, it leaves one massive elephant in the room: what do companies do with their vacant offices? A Savills Studley survey from 2016 showed that on average, most S&P 500 members spend between 1-2% of total revenues on rent. For a company making $100B in revenue, that is a ~$1.5B rent expense each year. If a company only expects to bring 25% of its employees back to the office full time, shouldn’t it look to reduce real estate costs?

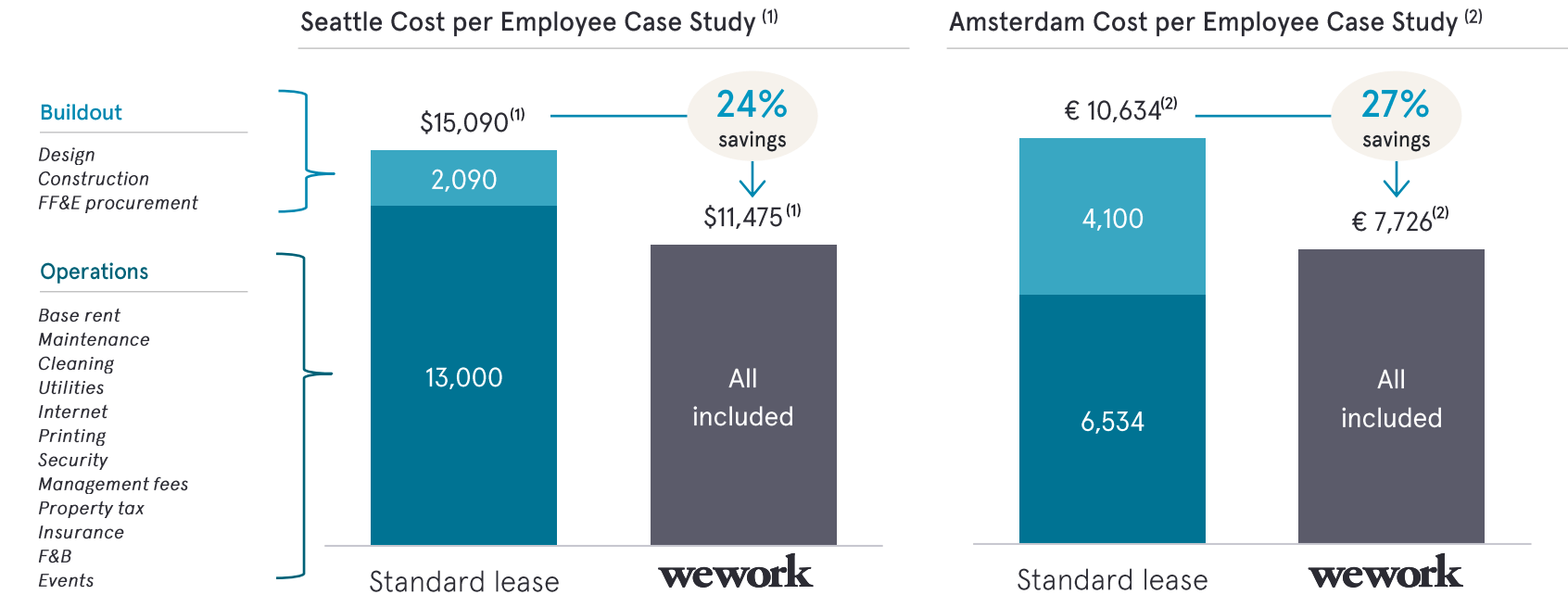

Source: WeWork Investor Presentation

WeWork conducted two case studies on the variance in cost per employee for customers leasing their own offices vs. using a WeWork location, and the data shows an average savings of 25% in both a US and European market. I expect flexible office solutions to increase in popularity as more enterprise customers realize the cost benefits vs. leasing their own real estate.

WeWork’s Surprise Pandemic Performance

In fall 2019, WeWork’s attempted IPO quickly became one of the more remarkable corporate implosions in recent memory. A prodigal CEO, laughable corporate governance, ridiculous cash burn rate, and a $47B valuation turned WeWork from “The next Alibaba” to a failing enterprise marred in scandal. So what happened since then? A global pandemic that should have put the nail in WeWork’s coffin actually gave the company a chance to prove itself once again. Similar to Airbnb (ABNB) outperforming expectations last year, WeWork’s resilient 2020 performance showed that hybrid and remote labor trends support the company’s business model.

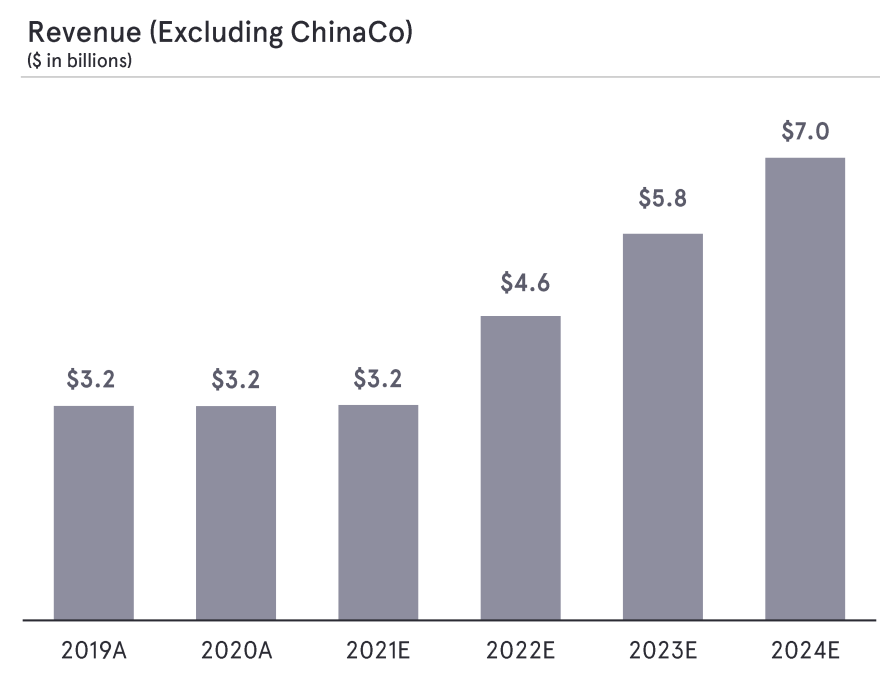

Source: WeWork Investor Presentation

WeWork managed to match its 2019 total revenue of $3.2B while navigating a pandemic and the fallout of its IPO failure. The popular narrative that office space would be crushed by COVID-19 did not apply to WeWork. Because WeWork was already structured to offer isolated workstations for individuals and enterprises alike, it could easily adapt to the challenges presented by the pandemic. The company was able to accommodate social distancing guidelines by rearranging workspaces, overhauling sanitation procedures, and adding additional barriers between workstations. Ironically, WeWork provided one of the few office solutions that could continue operating during a pandemic, making it a scarce commodity.

Enterprise Customer Growth

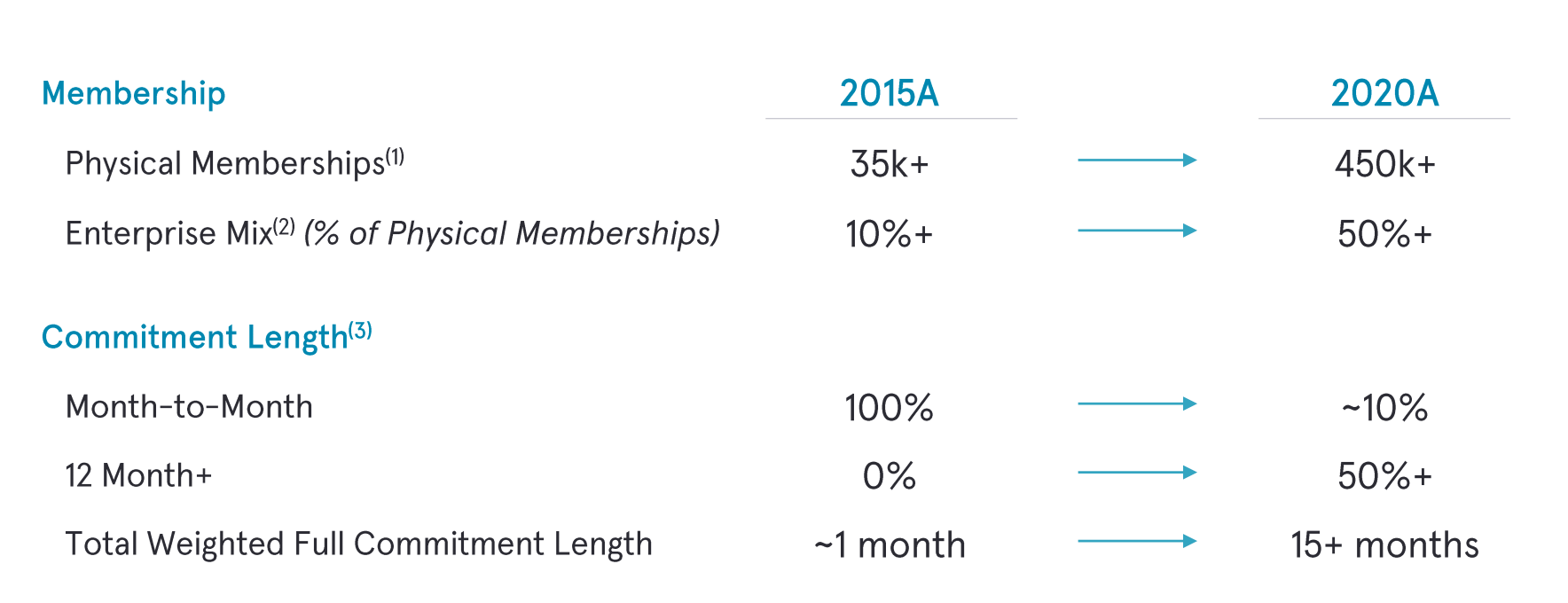

WeWork was able to keep its net revenues at $3.2B even while closing a number of locations (more on that shortly) thanks to an increase in enterprise customers (businesses with 500+ employees). When the pandemic forced startups to cut costs wherever possible, WeWork aggressively marketed itself to larger enterprises. As a result, more than 50% of the company’s current customer base comes from enterprises. Additionally, the average lease agreement is now over a year per customer, giving WeWork more stable annual cash flows.

Source: WeWork Investor Presentation

The company is targeting 65% enterprise customer composition long term, or a 15 point increase from the current level. WeWork also expects revenue growth to ramp up again starting next year, with the company projecting $7B in revenue by 2024. While stable revenue during the pandemic is a sign of confidence for the company, making money was never an issue for WeWork; burning billions a year was. However, WeWork’s new management has aggressively cut costs to lower cash burn and provide a realistic path to profitability.

Cost Cutting Initiatives

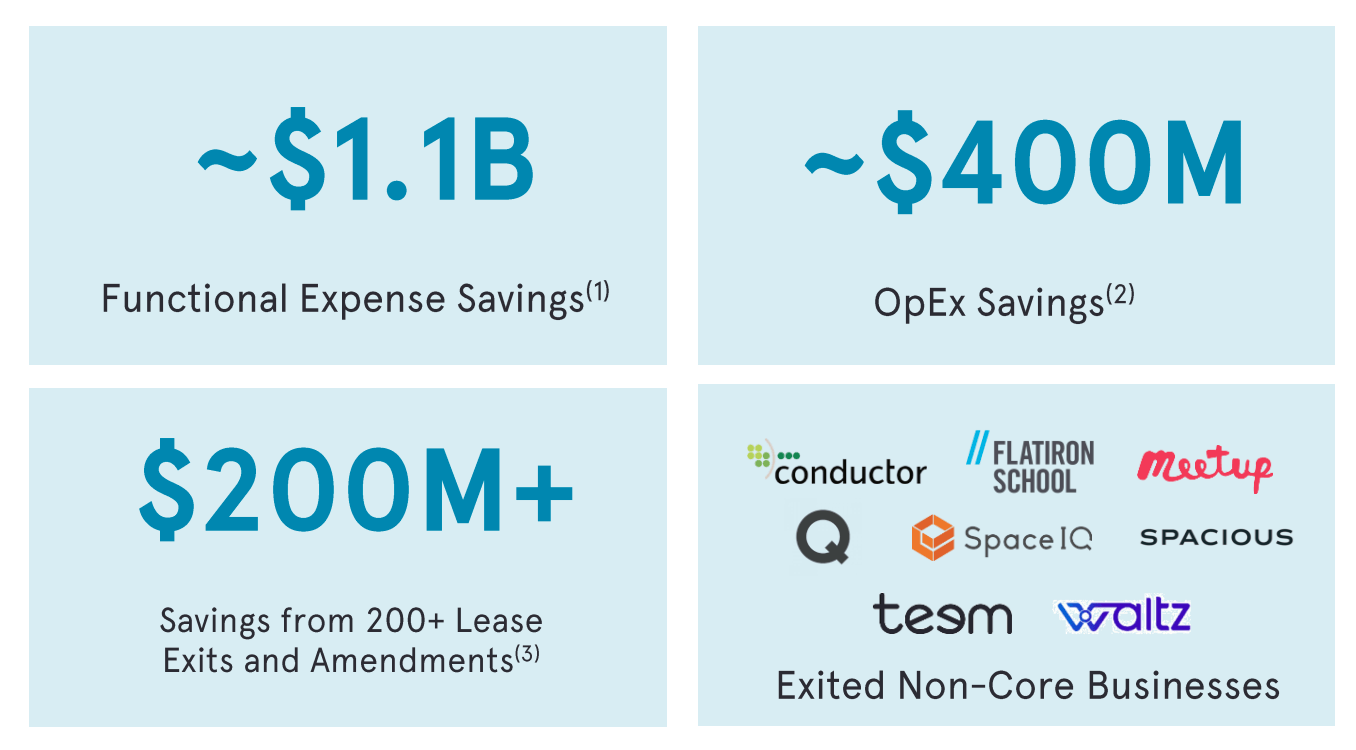

Source: WeWork Investor Presentation

Last year, WeWork laid off a third of its workforce, sold several non-core businesses including its China venture, exited 106 underperforming and unfinished office locations, and renegotiated 100 of its existing leases. These changes resulted in the savings in the graphic above. With these cost saving initiatives, WeWork is projecting $(0.9B) in 2021 Adj. EBITDA, a massive improvement compared to $(1.8B) in 2020 and $(1.9B) in 2019. Even more incredible, management now claims that the company will be profitable by Q4 2021. Additionally, WeWork believes it can maintain positive EBITDA margins as long as occupancy rates remain above 70% moving forward.

Source: WeWork Investor Presentation

Occupancy rates were depressed much of last year due to the pandemic, but rates appear to be trending back towards normalcy. IF (emphasis on if) WeWork can maintain positive EBITDA margins, the company’s biggest red flag becomes a nonissue.

Management Overhaul

Adam Neumann was the perfect individual to found and grow WeWork. A charismatic figure with a charming personality, Neumann appeared during the aftermath of the Great Financial Crisis with a unique idea that would appeal to venture capitalists across the country: Space as a Service. He painted WeWork as the future of a fluid, dynamic workforce, and his creation grew exponentially: at its peak, WeWork was worth $47B. As was the case here, the person needed to build a startup is rarely the best person to lead a mature company. When the company filed for an IPO, investors were wary of Neumann’s questionable business practices, such as borrowing money from WeWork to buy real estate that he then leased back to the company and charging WeWork millions to use his trademarked “We”. Neumann was also hemorrhaging billions a year on lavish company expenses, from over the top marketing campaigns, to a private jet, to needless office amenities.

The company pulled its IPO indefinitely in late 2019, and Neumann was asked to resign as CEO. The company concluded its search for a replacement by hiring Sandeep Mathrani, the perfect fit to lead WeWork out of this period of uncertainty. While Neumann treated the company as a next-generation tech unicorn, at its core WeWork is a real estate company dealing with leases, tenants, and debt. In 2010, Mathrani took over as CEO of General Growth Properties (GGP), one of the largest mall owners in the country, while the company was emerging from bankruptcy. Eight years later, Mathrani completed the turnaround by organizing a buyout by Brookfield Asset Management (BAM) to the tune of $15B. Mathrani is a veteran in the real estate industry, and he has a track record of success in rebuilding companies. In contrast to Neumann’s lavish management style, Mathrani is focused on building a profitable and respectable enterprise. The new CEO spearheaded the cost cutting initiatives mentioned above and refocused the company on its core competency: providing an affordable and flexible work environment to customers.

Benefits of the SPAC Model

WeWork going public through a Special Purpose Acquisition Company (SPAC) is the most ironic combination of 2021. A disgraced company paired with a risky merger vehicle should be a massive red flag, right? I disagree. For those unfamiliar with SPACs, they are publicly traded shell companies that provide an alternative method for private companies to go public. SPACs raise $X, put the money in a trust account, and then provide capital to their merger partner when the deal closes. In this case, BOWX is contributing $483M to WeWork for 6.1% of the company. BOWX shareholders will have their stock converted to WeWork shares once the merger closes. However, SPACs have a redemption clause that allows shareholders to redeem their shares for $10 and change. This creates a “floor” on the stock, where you have a maximum downside risk leading up to the merger. Additionally, SPACs have warrants that function similar to call options. In the case of BOWX, the warrants give you the right to buy one share of the stock at $11.50 for five years after the merger closes, and the company can redeem all warrants if they maintain a price of $18.50 or more. Right now, BOWX is trading at $12 and its warrants (BOWX/ws) are trading at $2.75. If WeWork reaches $20 post merger, the stock will increase by 66%, but the warrants will increase by 209% to $8.50 ($20 – $11.50). I view WeWork as a high risk, high reward investment. If the company does not perform, lease obligations and other expenses could eventually lead to its failure. However, if it hits its EBITDA projections, WeWork could prove to be a fantastic investment. Given the risk/reward dynamic, I find the warrants to be an interesting play. They provide much higher returns with the same loss if the stock drops to zero.

Risk Factors

No investment is risk-free, and I have highlighted some of the key risks to WeWork below:

- Inability to cover expensive lease obligations

- Occupancy rates remaining depressed for an extended period of time

- Slow adoption of flexible office solutions by enterprise customers

- Losing market share to competitors

- Understated variable costs that impact the ability to hit EBITDA targets

The first two risk factors are tied together, as the biggest determinant in WeWork’s ability to cover its expenses is occupancy rates. Assuming occupancy rates sustain 70% or more, WeWork should fine financially. However, a prolonged suppression of occupancy rates would severely hinder the company’s ability to pay its leases. That is the most important metric to watch in 2021. Additionally, there is no guarantee that large companies will continue turning to WeWork. Market conditions suggest that the trend will continue, but an unforeseen catalyst could upend the current trajectory. WeWork is the market leader in rentable workspace, but competitors such as Regus could cut into WeWork’s market share. Finally, an increase in variable costs such as marketing, general & administrative, or some other expense could impede the company’s ability to hit its EBITDA targets.

Summary

As mentioned before, this is a risky investment. I am betting that WeWork’s flexible work solution will appeal to many enterprise customers, and new management can keep the company on track to reach profitability. Execution risk is still high at this point, but uncertainty provides the best entry points. By the time we know whether or not WeWork will succeed, we may have missed a great investment opportunity. If you believe the company can take advantage of a post-COVID workforce, WeWork makes an intriguing investment.

Source: Seeking Alpha – WeWork: An Intriguing Investment For A Post-COVID Workforce